In 2020 Madrileña Red de Gas showed strong stability and great resilience over the course of what was an exceptional financial year. The company obtained excellent results, confirming its solid position and reliability to generate income. Revenue was €176 million with EBITDA of €139.7 million, figures that are lower than those recorded in 2019, although the fall in revenue was partially offset by an improvement in costs, as a result of operational efficiencies achieved over recent years.

5.1 RESULTS SUMMARY

Despite the pandemic, which left such a mark on 2020, MRG showed great stability and financial resilience, obtaining excellent results that confirm its solid position and reliability to generate income.

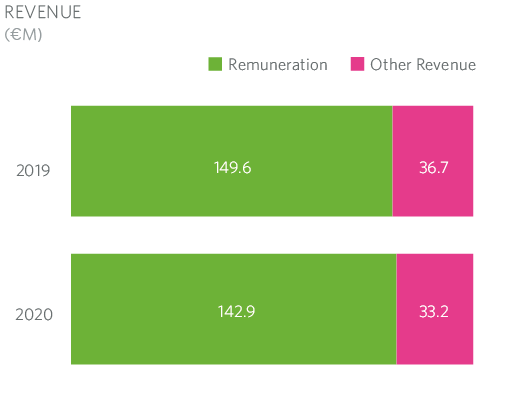

| M€ | 2019 | 2020 | 1 In accordance with the International Financial Reporting Standards (IFRS). 2 Excluding non-recurring expenses. |

| Remuneration | 149.6 | 142.9 |

| Other revenues | 36.7 | 33.2 |

| EBITDA2 | 145.9 | 139.7 |

| EBIT | 113.7 | 106.8 |

| Net profit | 65.0 | 64.4 |

Company revenue was €176 million, a 5% drop compared with 2019, and EBITDA of 139.7 million, a drop of 4% in relation to 2019. This fall in revenue and EBITDA is due mainly to a €6 million drop in remuneration and a drop in other revenue of €4 million compared with 2019.

Remuneration for distribution is the main source of revenue for MRG. It is calculated each year using a parametric formula and varies depending on the growth in supply points and demand conveyed through the network. A total of 99% of customers connected to the company’s network are residential. This means that MRG has remained stable in the face of economic cycles, as the temperatures in the colder months are what have the greatest impact on the final figure of the remuneration received. In 2020 temperatures in the Madrid region were higher than in 2019, and this is the main factor behind the drop in revenue from remuneration.

The company’s customer base continues to grow. At the close of 2020, Madrileña Red de Gas distributed gas to 912,670 supply points, of which 890,027 were for natural gas and 22,643 for LPG

The drop in other forms of income is due to the activity involved in carrying out regular inspections, which must be carried out every five years at every supply point in the company’s network, and these supply points are not spread out evenly between the five years. In 2020, a lower number of inspections needed to be carried out than in 2019, and this was the main factor behind the drop in other forms of income.

However, the fall in revenue was partially offset by an improvement in costs, as a result of operational efficiencies achieved over recent years.

The company’s growth strategy continues to be profitable and sustainable expansion in our territory and in adjacent territories. The company’s customer base continues to grow. At the close of 2020, Madrileña Red de Gas distributed gas to 912,670 supply points, of which 890,027 were for natural gas and 22,643 for LPG.

The main activity of MRG is the distribution of natural gas, which is a regulated activity. The regulatory periods for this activity are in six-year cycles, and 2020 was the last year in the period that began in 2014, a period of great stability. A new period begins in 2021, in which the regulatory framework has already been defined. Over the course of 2020 the methodology was published to calculated the remuneration. This methodology has the same approach as previously, but includes a gradual offset of revenue over the period. The offset finally published for MRG means an average cut of 10% in the regulatory period now under way, a similar figure to that applied to the main companies in the sector.

The consortium of company shareholders has not changed during the year. For them, MRG represents a long-term value creation project where they share the same strategic vision and a commitment to long-term financial strength.

Indeed, financial strength is one of the company’s mainstays, and MRG strives to maintain strong levels of solvency and liquidity consistent with the degree of investment to which the company is committed, balancing the cash flow-to-debt ratio.

5.2 OPERATIONAL RESULTS

In 2020, our EBITDA was €139.7 million, 4% lower than in 2019. Revenue fell by 5%, the main cause of which was the drop in EBITDA, which also showed lower costs due to operational efficiencies.

5.3 REVENUE

Total revenue in 2020 was €176 million, a 5% drop compared with 2019, due mainly to a lower demand for gas due to higher temperatures and a seasonal effect due to the lower number of inspections made compared with previous years.

A total of 98% of the company’s revenue stems from regulated activities. A total of 81% of this is revenue from distribution, legally recognised in the resolution of 18 December 2019 issued by the CNMC on the payment of companies conducting regulated activities relating to liquid natural gas plants, transport and distribution for the 2020 financial year, and the adjustments that have been made and estimated based on the evolving demand for gas. The remaining 19% refers to other services related to the distribution of natural gas, such as rental of meters, regular inspections, other consumer services and the sale and distribution of LPG.

5.4 FINANCIAL POSITION AND BALANCE

Financial strength is one of the strategic mainstays of the Madrileña Red de Gas. The company has strong levels of solvency and liquidity consistent with an investment grade rating. The financial structure is efficient and long-term. In 2020, gross debt amounted to €950 million with an average maturity period, at the close of 2020, of six years, approximately, and an average cost of 2.7%.

The company also has a contingent line of credit, which was reduced to €75 million during the first quarter of 2020, with the aim of achieving efficiencies in the financial infrastructure, adjusting the sum of said credit to the real needs of the company for the coming years.

Dividend flexibility is another feature that gives the company a better financial position.

The debt of the group is issued by MRG Finance in the regulated Luxembourg market under the EMTN Programme. This debt is classed as investment grade (BBB-) by Fitch Ratings, S&P Global Ratings and DBRS.

Financial strength is one of the strategic mainstays of the Madrileña Red de Gas. The company has strong levels of solvency and liquidity consistent with an investment grade rating

| M€ | 2019 | 2020 | 1 In accordance with the International Financial Reporting Standards (IFRS). |

| Gas distribution licences & other intangibles | 751.0 | 751.0 |

| Net tangible fixed assets | 354.9 | 339.2 |

| Total network fixed assets | 1,105.8 | 1,090.2 |

| Goodwill | 57.4 | 57.4 |

| Deferred tax assets | 21.5 | 17.9 |

| Other non-current assets | 55.7 | 212.1 |

| Current assets | 42.3 | 47.7 |

| Cash | 103.4 | 46.6 |

| Total assets | 1,386.2 | 1,417.9 |

| Equity | 298.1 | 362.5 |

| Long term debt | 943.8 | 945.2 |

| Deferred income tax liabilities | 60.1 | 70.0 |

| Other non-current liabilities | 37.5 | 38.6 |

| Current liabilities | 46.7 | 55.6 |

| Total liabilities & shareholders equity | 1,386.2 | 1,417.9 |

5.5 OPERATIONS CASH FLOW

Cash flow was €133.9 million, 16% up from 2019. The main difference is due to greater investment in working capital in 2019 due to the end-of-year position of settlements with the system.

SThe cash flow calculation does not include non-recurring operational items, such as the settlement with Naturgy for the losses corresponding to the years when the network was not sectorised, and the cash revenue from the enforcement of the judgement on the Castor underground storage during the 2019 financial year, as well as outgoing cash flow for the same amount and concept in 2020 to the banks that own the deficits from previous years.

| M€ | 2019 | 2020 | 1 In accordance with the International Financial Reporting Standards (IFRS). 2 Excluding one-off operations (incoming payment of the Castor project in 2019, plus the payment made for losses in previous years). |

| EBITDA | 145.9 | 139.7 |

| Income tax paid | (6.9) | (7.1) |

| Working capital2 | (10.5) | 15.5 |

| Capex | (13.5) | (14.3) |

| Free cash flow2 3 | 114.9 | 133.8 |

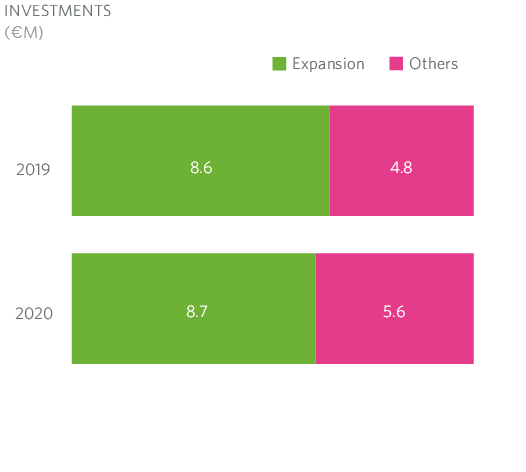

5.6 INVESTMENTS

In 2020, investment amounted to €14.3 million, an increase of 6% compared with 2019. These investments can be divided into the following groups:

Expansion

MRG invested a total of €8.7 million in expanding its network, in alignment with the amount invested in 2019 and with its strategy of viable and sustainable expansion.

Other projects

Investment was also made in a range of other projects, such as maintenance, AI tools, digitalisation, automating processes and developing information systems that are aimed at reaching our targets of cost efficiency and improvements in the quality of our customer service.

In 2020, investment amounted to €14.3 million, an increase of 6% compared with 2019